No, China has not stopped investments into VIEs

No, China has not stopped investments into VIEs

They appear to have stopped companies creating offshore listing structures, which is an entirely different and potentially broader problem.

As the Chinese government’s new Age of Regulation continues to spook investors into guessing what the next big move might be, it’s interesting to see the discussions started by any news to hit Twitter.

One such instance is the reports that the Shanghai government was stopping investments into VIEs. It’s really interesting to me for two reasons:

Firstly, the Shanghai government haven’t stopped investments into VIEs, they seem too have stopped investments into offshore listing structures. These are definitely related to VIEs, but this move has implications for companies that don’t use VIEs as well.

Secondly, looking at the potential impact of an actual stop to investments/money flows into VIEs is interesting, and this type of move would have a very wide range of impacts based on how well the company has structured its VIEs.

In, not out

The key early indicator that the moves from the Shanghai regulators aren’t stopping investments into VIEs is that they are stopping outbound investments into the Cayman’s. As we know from earlier the Cayman company is not the VIE, which is an entity incorporated in China.

So if you’re stopping investments into the VIE, you’re actually stopping inbound investments or money-flows, not outbound. But more on this later.

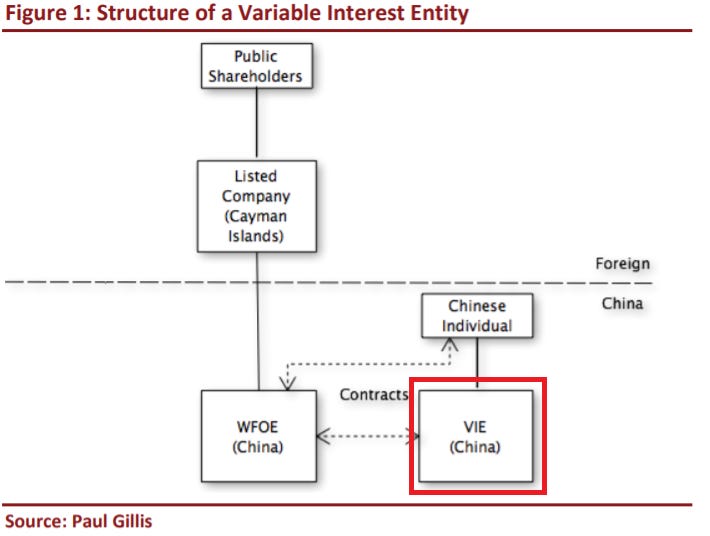

It’s useful to take a bit of a deeper dive here into the difference between the VIE structure, and the offshore listing structure. These are often confused with each other as we have seen, and the offshore listing structure is sometimes included in the discussions about the VIE structure.

If we look at the corporate structuring of Chinese companies listed abroad that use VIEs, there are actually two parts to the setup. The VIE is there as a workaround to the foreign investment rules, and the offshore listing structure is there as a workaround to Chinese rules related to floating the shares on an exchange.

The VIE structure is actually an entirely onshore affair. When we’re discussing what the VIE structure is, and what risks are related to it, how they’re managed and governed, what we’re really discussing is the relationship between the VIE entity, and the Listco’s wholly owned subsidiaries (WFOEs) in China.

The core of the VIE structure is the contractual control element between the WFOE and the VIE entity, but operationally and from a risk perspective it’s also important to look at how the VIEs operate together with the WFOEs. A well-managed VIE structure will tend to have most assets, and revenues handled in the WFOEs instead of the VIE, for instance, so that these are under the direct control of the foreign shareholders in the Listco.

Notice that this entire discussion is still related to onshore activities, the problem is that you’re unlikely to be able to get approval to list this overseas. In fact there are plenty of companies that don’t use VIEs at all (ie they’re not operating in negative list industries) that have this very same problem. It has traditionally been very hard to get approval to list shares of your Chinese entity abroad.

So, this requires another, separate workaround. Luckily this workaround is a bit more straightforward.

While you can’t list your Chinese company overseas without approval, if the Chinese company was taken over by a Cayman Island company they wouldn’t need to apply for permission to list. So the standard setup was created to establish an offshore structure for listing overseas, and it’s the establishment of these entities that the Shanghai government has stopped (or rather the reorganisation of them that established the ownerships etc.).

So, while the reported regulatory actions definitely does impact companies using VIEs, it’s very likely that it actually shuts down the establishment of offshore listing structures for all applicants. This essentially stops the now standard way for most Chinese companies to list abroad, although it could be that the Shanghai authorities are being more granular than this.

This also means that the impact of this could potentially be much broader, and more in line with the CSRCs recent statement that they want to firm up listing procedures overall.

But, what if?

Banning money-flows into VIEs would be a very different endeavor, it would have a narrower but potentially deeper impact, and some of the groundwork for it has been around for a long time.

Getting money into VIEs isn’t actually all that straightforward in the first place. I first wrote about this issue with Shoushuang Li back in 2011, and while we have of course moved on somewhat since then the core issues remain.

Moving money into a company you don’t control, in an industry you’re technically limited from engaging in is always going to throw up some challenges. In fact, there are risk disclosures about the potential inability of moving the money raised offshore into the VIE in most filings from Chinese companies using the structure.

PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent us from using the proceeds of this offering to make loans or additional capital contributions to our PRC subsidiary, our VIEs and their subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business.

We are an offshore holding company conducting our operations in China through our PRC subsidiaries, our VIEs and their subsidiaries. We may make loans to our PRC subsidiaries, our VIEs and their subsidiaries, or we may make additional capital contributions to our PRC subsidiaries, or we may establish new PRC subsidiaries and make capital contributions to these new PRC subsidiaries, or we may acquire offshore entities with business operations in China in an offshore transaction.

Most of these ways are subject to PRC regulations and approvals or registration. For example, loans by us to our wholly owned PRC subsidiary to finance its activities cannot exceed statutory limits and must be registered with the local counterpart of SAFE. If we decide to finance our wholly owned PRC subsidiary by means of capital contributions, these capital contributions are subject to registration with the State Administration for Market Regulation or its local branch, reporting of foreign investment information with the Ministry of Commerce, or registration with other governmental authorities in China. Due to the restrictions imposed on loans in foreign currencies extended to PRC domestic companies, we are not likely to make such loans to our VIEs, which are PRC domestic companies. Further, we are not likely to finance the activities of our VIEs by means of capital contributions due to regulatory restrictions relating to foreign investment in PRC domestic enterprises engaged in certain businesses.

…

In light of the various requirements imposed by PRC regulations on loans to and direct investment in PRC entities by offshore holding companies, we cannot assure you that we will be able to complete the necessary government registrations or obtain the necessary government approvals on a timely basis, or at all, with respect to future loans to our PRC subsidiaries or VIEs or future capital contributions by us to our PRC subsidiaries. As a result, uncertainties exist as to our ability to provide prompt financial support to our PRC subsidiaries or VIEs when needed. If we fail to complete such registrations or obtain such approvals, our ability to use the proceeds we expect to receive from this offering and to capitalize or otherwise fund our PRC operations may be negatively affected, which could materially and adversely affect our liquidity and our ability to fund and expand our business.

It’s a bit of a mouthful, admittedly.

But since it’s hardly a straightforward issue to begin with, it’s not too much of a stretch to imagine there being some scrutiny coming to the topic. Some might argue it’s a bit strange that we haven’t seen anything so far, but then others would say that’s a good indication that the relevant authorities are OK with it.

And while the restrictions on establishing offshore listing structures don’t really matter to the companies already listed, this would be another matter entirely.

Companies would be unable to move any money raised or held overseas into their VIEs, and if you’re a company that primarily operates through your VIE this would be a big problem. More well managed companies like Alibaba would likely still do OK, since they directly own and control the vast majority of their assets and revenues through their WFOEs. Meaning they’re unlikely to be limited in their ability to transfer money to their operational subsidiaries, but not all companies are structured so well.

As we can see, limits on establishing offshore listing structures and limits on money-flows into VIEs are very different both by their nature, and regarding what types of issues they generate. While the currently reported one is likely to affect all Chinese companies looking to list overseas in the future, stopping money-flows into VIEs would have a direct, and potentially material impact, on companies listed now.